At what level does a statutory royalty administrator begin wanting much less like a collective licensing entity and extra like an unregistered funding fund or small financial institution?

That query is changing into not possible to keep away from. Until you’re studying the trades or going to business conferences when you possibly can keep away from it simply superb.

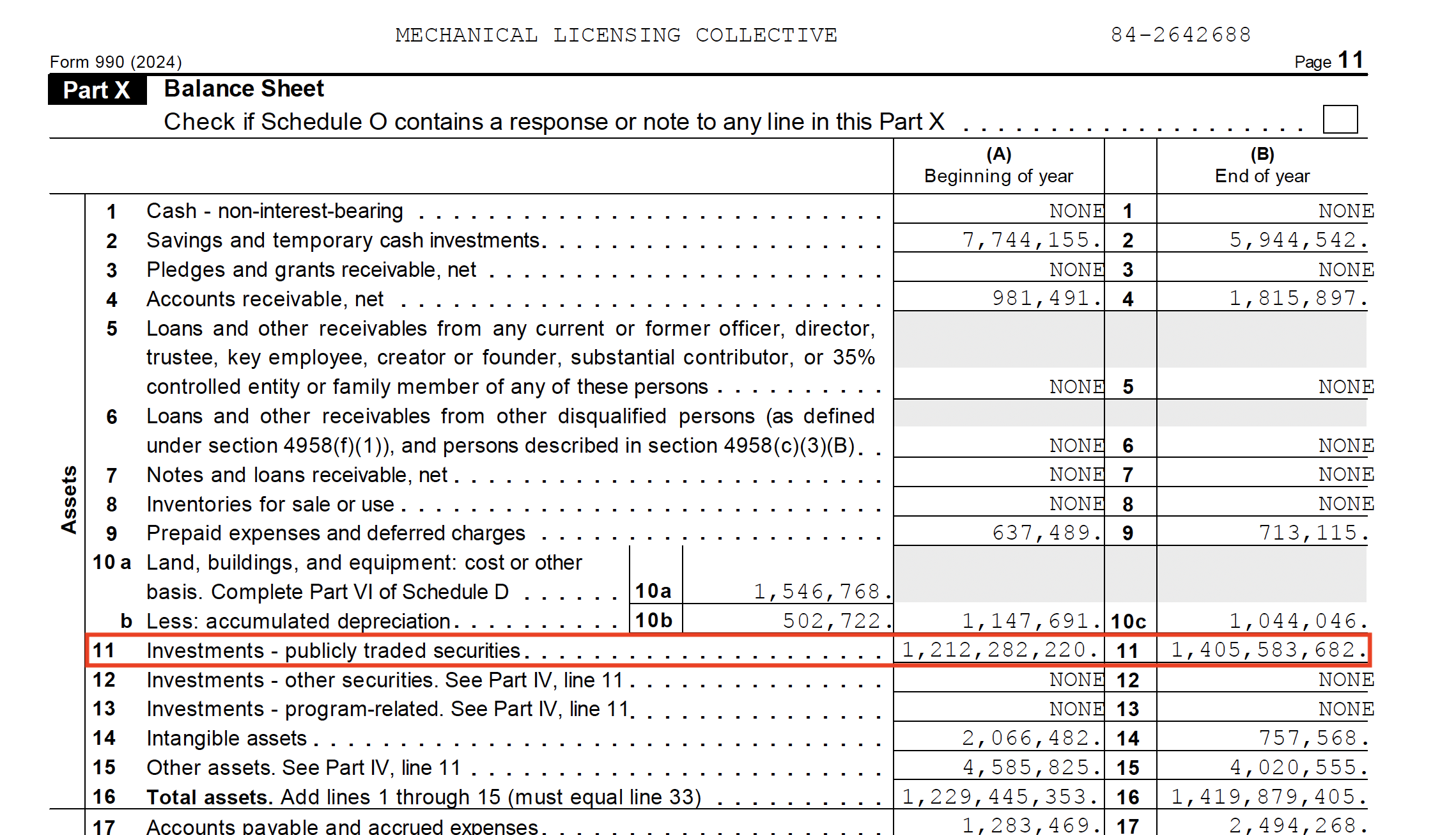

The MLC isn’t merely holding just a little float whereas it figures out who to pay. Its 2024 tax return reviews roughly $1.4 billion in publicly traded securities—a securities portfolio massive sufficient to exceed the entire asset base of many neighborhood banks and to sit down close to the federal CRA threshold for a “small financial institution.” That isn’t administrative pocket change. That’s different individuals’s cash at financial institution scale, with out bank-style supervision. Or actually any supervision in any respect.

If a neighborhood financial institution held $1.4 billion in belongings, regulators would care very a lot about its funding coverage, custody, liquidity, conflicts, governance, and disclosure in contrast to the U.S. Copyright Workplace which is charged with MLC oversight however has by no means as soon as taken a place concerning the huge unmatched holdings. The most important distinction between the MLC and a financial institution is that this “black field” cash belongs to copyright homeowners the MLC says it may possibly’t find, not depositors—and the statutory guardrails seem thinner, not stronger.

The MLC’s pooled royalty portfolio presents exactly the sort of different individuals’s cash downside the Funding Firm Act of 1940 was designed to police. The core concern isn’t merely that cash is invested. The priority is that one establishment controls pooled belongings belonging beneficially to others (though not of their possession), makes use of these belongings in securities markets, and does so with out the bizarre protections of consent, disclosure, redemption rights, portfolio transparency, or significant beneficiary management. After all so far as we all know, the MLC doesn’t provide its personal securities to the general public, which might preserve them out of 40 Act compliance strictly talking.

But unknown copyright homeowners are particularly weak. They didn’t select the MLC. They didn’t authorize its funding coverage. They can not monitor trades. They can not consider threat. They can not vote with their ft. Their royalties entered the system by federal compulsion after which grew to become half of a big institutional pool managed by individuals they could by no means have heard of. Assuming that these are all DIY artists who assume they co-wrote Yesterday as a result of they lined it or that by some means it’s the songwriter’s fault as a result of they didn’t “Hook up with Gather” is artist-shaming at its worst. The large salaries at MLC ought to inform you that Congress expects these executives to do their jobs and discover these individuals. They’ve had years to do it already and but…$1.4 billion in securities, up $200,000,000 in 2024 alone.

That’s precisely one hazard the 1940 Act was meant to handle: insider administration of different individuals’s cash underneath opaque situations. The MLC could argue that its major enterprise is royalty administration, not funding administration. But when the MLC holds over $1.4 billion {dollars} in publicly traded securities—which it does—generates positive aspects and losses from buying and selling—which it does—depends on monetary advisors—which it does—and resists portfolio disclosure on market-timing grounds—which it does—the SEC and Copyright Workplace ought to ask whether or not 1940 Act rules ought to use even when the MLC doesn’t promote its personal securities.

At minimal, these rules require disclosure, segregation, fiduciary accountability, and safety of the absent homeowners whose cash made the portfolio doable within the first place.

The Mechanical Licensing Collective was created by Congress underneath Title I of the Music Modernization Act to manages the musical works database (which is on the coronary heart of this downside), administer the blanket mechanical license, accumulate royalties from digital providers, match works to homeowners, and pay songwriters and publishers. The MLC was not offered to Congress as a hedge fund.

There’s a tendency to overstate the difficulty. The MMA did authorize the MLC to obtain historic unmatched royalties transferred by DSPs throughout the transition to the blanket license regime. The authority comes principally from 17 U.S.C. § 115(d)(10) and implementing rules at 37 C.F.R. § 210.10. The primary distribution of the “historic unmatched” included royalties from not less than 5 digital service suppliers. These funds had been particularly for makes use of that occurred throughout the Phonorecords II charge interval, which spans from January 1, 2013, to December 31, 2017. The preliminary complete transferred by DSPs was about $424,384,786.63 (adjusted later to roughly $397,271,958.10 after unexplained subsequent charge changes). The MLC claims that roughly 58% of that sum has been distributed (presumably matched), which makes the $200 million YOY improve of their 2024 holdings of public securities even tougher to clarify.

Which begs the tougher query: What authority did Congress gave the MLC to deal with these huge sums after it obtained the historic and present unmatched royalties? Was the belief that they’d discover the songwriters whose cash they obtained paid?

Title I of the MMA speaks by way of holding accrued royalties in an interest-bearing account and crediting curiosity to the advantage of “copyright homeowners entitled to fee of such accrued royalties.” The MMA does not say the MLC could function an unregulated billion-dollar actively managed securities portfolio utilizing unmatched royalties collected underneath federal compulsion.

But the MLC’s publicly filed 2024 tax return additionally disclosed $72 million in funding earnings for 2024, up from a mere $51,757,502 in 2023. That’s virtually double the $39,050,000 administrative evaluation for 2024 which is paid by the licensees underneath the auspices of the Digital Licensee Coordinator (DLC). You do should marvel if the MLC’s funding earnings ought to have some connection to the executive evaluation. Perhaps not, but when I’m a licensee, I’m questioning about that.

I feel that’s the place the actual problem begins. Who owns the buying and selling earnings? Who bears the losses? These questions usually are not peripheral accounting particulars. They go to the guts of the MLC’s authorized authority and fiduciary obligations.

If unmatched royalties beneficially belong to unknown songwriters and publishers, then one may fairly ask why positive aspects generated from investing these funds usually are not allotted transparently to the helpful homeowners whose cash generated the returns. If this cash was handled like different unclaimed property, it will be transferred to a Secretary of State to be held eternally till the proprietor (the unknown copyright proprietor) could possibly be discovered. However the lobbyists drafted Title I of the Music Modernization Act in order that it purports to preempt state unclaimed property legal guidelines, concentrating management over unmatched royalties on the MLC. That centralization heightens fiduciary issues, as conventional escheat protections for unclaimed property are displaced, growing the danger that undistributed funds are managed with out sufficient accountability to the true copyright homeowners. (I’m not 100% satisfied that preemption is Constitutional, however that’s a subject for one more day.)

If the buying and selling earnings belong to the MLC itself, the place did the MLC get hold of statutory authority to take a position with different individuals’s royalty cash for its personal institutional profit? If the positive aspects scale back future administrative assessments payable by DSPs, then songwriters could successfully be subsidizing licensees by involuntary use of unmatched royalties. And if the portfolio suffers losses, who absorbs the shortfall? Copyright homeowners? DSPs? Administrative assessments? Songwriters have by no means obtained a transparent reply.

The statutory language turns into much more troubling when one focuses on the phrase “copyright homeowners entitled to fee.” The MMA offers that unmatched royalties shall be maintained in an interest-bearing account and that the curiosity “accrues for the advantage of copyright homeowners entitled to fee.” However who precisely are the “copyright homeowners entitled to fee”?

Does that phrase imply the precise homeowners of the unrivaled works whose cash the MLC did not distribute in a well timed method and who subsequently obtain the statutory curiosity as a sort of penalty or compensation for delay and incompetence? Or does “copyright homeowners entitled to fee” by some means embrace the massive market-share recipients who could obtain distributions from the unrivaled pool years later, like underneath the MLC’s introduced 2027 black-box distribution course of?

That distinction issues enormously as a result of it goes on to ethical hazard. If the MLC or the broader business understands that unmatched royalties and related funding positive aspects will finally circulation out by market-share distributions to main incumbents, does that strengthen or weaken the motivation to aggressively enhance matching efficiency of the MLC?

The statutory curiosity provision ought to function as a penalty for failure to match and distribute royalties promptly just like the late payment for late fee by DSPs, not as an financial reward for sustaining a big unmatched reservoir of different individuals’s cash.

Why shouldn’t the curiosity penalty come out of the MLC’s personal working funds or administrative assessments quite than from unmatched royalties themselves? If the curiosity obligation got here straight out of the MLC’s administrative evaluation, the licensees paying that evaluation would all of the sudden have a really sturdy incentive to ensure the actual copyright homeowners obtained discovered shortly. Beneath bizarre fiduciary rules, a trustee or administrator typically doesn’t revenue from delays in distribution of beneficiary funds.

The longer this problem goes unanswered, the tougher it turns into to keep away from the looks that the unrivaled pool has quietly developed from a short lived custodial downside right into a everlasting monetary asset.

The MLC’s personal explanations have solely deepened the priority. In an ex parte submission to the Copyright Workplace, commenters pointed to statements by the MLC suggesting that disclosure of portfolio particulars might expose the group to market-timing issues as a result of public data about massive trades may have an effect on execution.

We’re now not speaking about passive custodial money administration. We are actually speaking a few federally created collective asserting issues that sound remarkably just like these raised by institutional funding managers executing massive securities trades.

In some unspecified time in the future the plain query emerges: has the MLC drifted into conduct functionally resembling a hedge fund?

The MLC would undoubtedly argue that its major function is royalty administration, not investing, and that funding exercise is merely incidental to holding unmatched royalties pending distribution. However that’s not what their tax returns inform you. And the response doesn’t finish the inquiry.

The MLC is reportedly investing monumental sums in publicly traded securities. It’s utilizing exterior monetary advisors. It’s producing positive aspects and losses. It’s discussing market-moving trades. It’s pooling (and probably co-mingling) cash belonging beneficially to others who didn’t consent to the funding technique.

At minimal, the SEC and Copyright Workplace ought to decide:

– whether or not the MLC’s funding actions are approved underneath the MMA,

– whether or not any exemption from monetary regulation is being relied upon,

– whether or not unmatched royalties are being commingled with administrative assessments or operational funds,

– how positive aspects and losses are allotted,

– whether or not portfolio earnings belong beneficially to copyright homeowners,

– and whether or not the MLC has assumed fiduciary obligations exterior the statutory framework Congress created.

The fiduciary problem could in the end be essentially the most harmful one. By voluntarily adopting an funding coverage not expressly required by the MMA (and I’d say not permitted by Congress, both), the MLC could have assumed duties analogous to a trustee holding and investing property for beneficiaries. Which raises one other uncomfortable query: what did the board know? Who permitted the funding coverage? Did exterior securities counsel evaluation it? Was the SEC consulted? Did board members ask who would obtain buying and selling earnings or take in buying and selling losses? Did nonvoting board contributors object or approve the funding coverage? Did anybody search formal Copyright Workplace approval earlier than the MLC started working what more and more resembles a big institutional portfolio?

Name me cynical, however I’d put cash on the reply to all these questions being a powerful “no.”

The MLC was created to pay songwriters. To not turn out to be a billion-dollar opaque buying and selling operation utilizing compulsory-license royalty flows collected underneath federal authority.

{kind=link}