Why the Most Essential AI Query Could Not Be About AI at All

Don’t Fear, Be Blissful

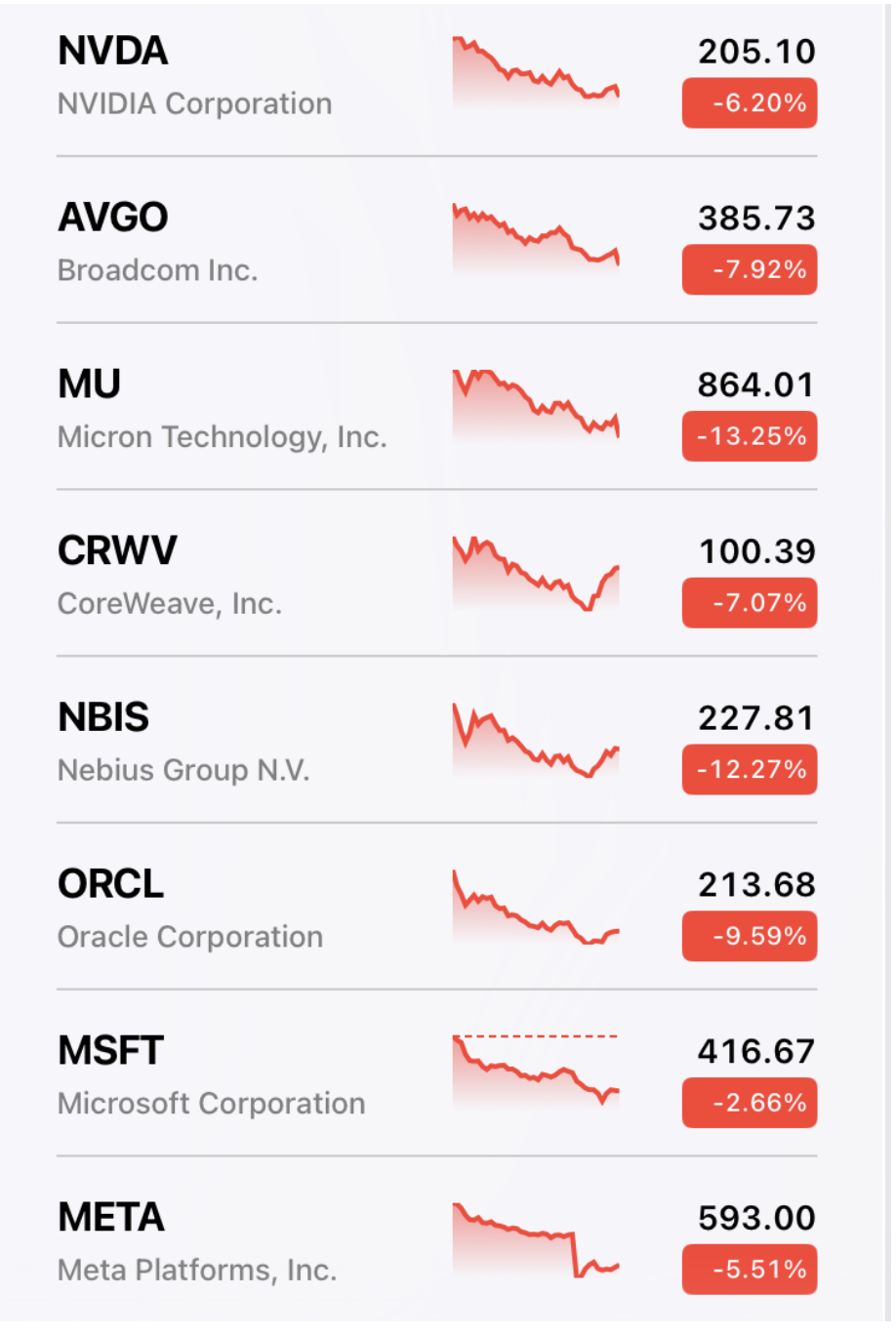

Markets go up and down, can’t decide a high, can’t decide a backside however….what a distinction a day makes. Friday’s sell-off in AI-related shares seems to have mirrored at the least a second of reflection if not a rising realization that the business’s economics stay largely unproven. Buyers are starting to query whether or not huge capital expenditures on chips, knowledge facilities, transmission infrastructure, and energy era might be justified by future revenues. Considerations about token pricing, enterprise adoption prices, and the eventual expiration of backed pilot applications have raised doubts about long-term profitability. On the similar time, looming IPOs, inevitable lockup expirations from these IPOs, and the prospect of elevated disclosure relating to AI working prices have shifted consideration from progress narratives towards fundamentals, money move, and return on invested capital.

A lot of the general public debate surrounding synthetic intelligence focuses on theft of tradition, AI fashions, valuations, copyright disputes, regulation, eminent area pushed knowledge middle development from all these good cyber-libertarians in Silicon Valley, and the eventual public choices of firms corresponding to OpenAI, Anthropic, and xAI. These points are necessary, however they might not be essentially the most consequential questions going through buyers, policymakers, ratepayers, pension beneficiaries, or native communities.

The defining monetary attribute of the present AI buildout might not be valuation, leverage, and even know-how. It could be length mismatch—the rising hole between capital dedicated right this moment and money flows anticipated to reach years and even a long time into the long run. In the event that they arrive in any respect. And all the info middle development corruption within the universe can’t overcome the physics of cash.

That distinction is essential as a result of whereas the capital expenditures are observable right this moment, the returns on funding (the dreaded ROI) are undoubtedly not observable and even quantifiable.

Knowledge facilities are being constructed right this moment. Chips are being bought right this moment. Energy contracts are being signed right this moment. Transmission corridors are being authorised right this moment. Utility investments are being deliberate right this moment. Tax incentives are being granted right this moment. Debt is being issued right this moment. Fairness is being diluted right this moment—even Google has run out of free money move for AI capex. The corresponding returns stay largely embedded in forecasts (also called bets) that make about as a lot sense as J. Wellington Wimpy’s cost on Tuesday for a burger right this moment.

Put in another way, the ROI is at present a speculation relatively than an observable financial reality.

This isn’t essentially a criticism of synthetic intelligence. Each transformative know-how requires funding earlier than it generates significant returns. Railroads required funding earlier than they moved freight. Electrical programs required funding earlier than they powered factories. Fiber-optic networks required funding earlier than they carried web site visitors. The business web itself required years of spending earlier than buyers may reliably measure its financial affect.

The query just isn’t whether or not AI will create worth. The query is whether or not demand arrives on the timetable assumed by right this moment’s capital allocation selections. That may be a basically totally different query, and it might finally show extra necessary.

However don’t fear, be pleased.

The Market Has Already Financed A lot of the AI Future

One widespread false impression is that the AI increase nonetheless lies forward as a result of a number of main AI firms stay personal. That view confuses financing occasions with financial actuality, and competence with IPOs (which are literally VC exits greater than the rest).

Going public and technological maturity have, at finest, a passing relationship. Fifteen or twenty years in the past, firms of OpenAI’s or Anthropic’s scale would probably have entered public markets a lot earlier. In the present day, personal capital markets have developed to offer liquidity via secondary transactions, growth-equity funds, sovereign wealth funds, crossover buyers, feeder autos, and more and more complicated SPV buildings that function largely within the secondary market.

In lots of circumstances, firms can receive the financial advantages of public-company scale with out changing into public reporting firms. (And sure, the SEC permits that to occur.). The result’s that a lot of the AI future has already been financed.

Public markets have poured trillions of {dollars} into NVIDIA, Microsoft, Alphabet, Amazon, Meta, Broadcom, AMD, Micron, TSMC, utilities, and data-center REITs. Hyperscalers have dedicated tons of of billions of {dollars} to knowledge facilities, networking tools, customized silicon, acquisitions, and energy procurement. Suppliers all through the ecosystem have expanded capability based mostly upon the identical assumptions.

In a way, the market has already IPO’d a lot of the AI story. The related query is subsequently not whether or not OpenAI ultimately recordsdata an S-1. The related query is whether or not the assumptions underlying the investments already made all through the ecosystem are right. Not like mature public firms, most of the most vital AI corporations function with restricted public disclosure regardless of attracting valuations corresponding to publicly traded issuers. In consequence, buyers, lenders, ratepayers, and policymakers are being requested to commit tons of of billions of {dollars} in money and authorities mortgage ensures or tax abatements based mostly on comparatively sparse info. This creates a considerable financial danger: if the underlying assumptions relating to demand, token consumption, profitability, infrastructure utilization, or future revenues show inaccurate, the ensuing correction may reverberate all through monetary markets, utility programs, and the broader financial system.

We’re means past Dot Bomb, railroads, and the Nice Monetary Disaster. Due to knowledge middle development and its harmful nature, the whole U.S. financial system might be affected.

When Software program Firms Develop into Infrastructure Builders

What makes the present cycle traditionally uncommon just isn’t merely the amount of cash being spent. It’s who’s spending it. Alphabet, Amazon, Microsoft, and Meta are among the many most worthwhile firms in human historical past. For many years, buyers rewarded these companies as a result of they mixed extraordinary margins with comparatively asset-light economics. Synthetic intelligence is altering that equation.

More and more, hyperscalers resemble infrastructure builders relatively than conventional software program firms. Governments are granting or facilitating extraordinary powers—together with transmission easements, utility price restoration, tax incentives, and in some circumstances entry to eminent-domain-backed infrastructure corridors—to help AI-related improvement. In impact, these firms are being handled much less like personal know-how distributors and extra like quasi-governmental entities (what Brits name “quangos”). But the extent of public disclosure stays far under what would ordinarily accompany investments of this magnitude. If the assumptions underlying demand, utilization, and profitability show incorrect, the financial penalties could lengthen properly past shareholders to landowners, ratepayers, taxpayers, and full rural communities.

A whole bunch of billions of {dollars} are being allotted to knowledge facilities, chips, networking tools, cooling programs, energy procurement, transmission entry, and associated belongings. These investments could finally show sensible or silly. The difficulty just isn’t whether or not the spending is justified. The difficulty is whether or not the timing of the spending aligns with the timing of the returns and what it means if there’s a mismatch (which I argue there already is).

From a corporate-finance perspective, the problem is easy. Capital expenditures happen instantly. The revenues used to justify these expenditures arrive later (which is why many, if not all, of the info middle construct is finished with debt or tax incentives created with the promise of future “jobs”).

The longer the hole between expenditure and monetization, the better the sensitivity to forecasting errors, rates of interest, utilization assumptions, technological modifications, and shifts in buyer demand. That is the essence of length mismatch.

The money outflows are actual and measurable. The money inflows stay contingent. The AI buildout subsequently resembles a long-duration infrastructure venture whose economics rely closely upon future utilization charges.

That ought to sound acquainted. It’s precisely what number of historic infrastructure cycles developed: formidable forecasts, considerable capital, authorities help, and widespread confidence that future demand would justify current funding. The railroad increase of the nineteenth century was constructed on the belief that westward enlargement and commerce would take in just about limitless rail capability. The electrification applications of the early twentieth century rested on forecasts of ever-growing industrial and residential demand. The dot-com telecommunications buildout of the late Nineties produced monumental investments in fiber-optic networks based mostly on expectations of web site visitors that finally arrived years later than anticipated. In every case, the infrastructure itself proved helpful. The tough query was whether or not the timing, scale, and financial assumptions underlying the funding have been right.

So sure, in the long term, the capital prices most likely labored out, notably when you bought a reduction by shopping for stranded belongings out of chapter. However as Professor Keynes as soon as mentioned :

This future is a deceptive information to present affairs. In the long term we’re all lifeless. Economists set themselves too simple, too ineffective a activity if in tempestuous seasons they’ll solely inform us that when the storm is long gone the ocean is flat once more.

The query just isn’t whether or not demand could ultimately arrive. The query is whether or not it arrives earlier than the capital construction collapses.

The Railroad Lesson

The railroad increase is usually remembered as a triumph of American capitalism (celebrated on Nob Hill on the Large 4 restaurant within the Huntington Hartford Resort). It was all of that.

It was additionally a graveyard for buyers. The error many trendy observers make is assuming that profitable applied sciences mechanically produce profitable investments. Historical past demonstrates in any other case. Railroads remodeled the American financial system. They opened new markets, lowered transportation prices, and accelerated industrialization.

But numerous railroad buyers misplaced fortunes. Why? As a result of capital (aka suckers) arrived quicker than demand. Infrastructure was constructed years earlier than utilization charges justified the funding. The know-how succeeded. The timing failed. The buyers ate it in a pre-SEC world (much like the one created by the distorted enlargement of secondary markets).

The identical sample appeared within the fiber-optic increase of the late Nineties. The world ultimately wanted monumental quantities of fiber. Buyers merely constructed an excessive amount of of it too rapidly. Once more, the know-how succeeded however the timing was a bitch when you invested too early. For instance, after the dot-com crash, Google was capable of purchase low cost “darkish fiber” (unused fiber optic cable) left behind by the telecom overbuild. That didn’t merely decrease its bandwidth prices; it helped flip Google from an internet site into a non-public infrastructure firm with CDN-like management over knowledge motion.

AI could finally observe an identical path. The know-how may match. The demand could arrive. The income could materialize. Buyers should lose cash if the forecasted money flows arrive later than anticipated. That distinction is essential as a result of the hazard just isn’t essentially technological failure or not solely that failure. The hazard is that capital markets as soon as once more show directionally right and temporally incorrect. I’d argue that has already occurred and can proceed occurring at an growing charge.

Certainly, there’s even a robust argument that this course of has already begun. The latest volatility in AI-related securities means that markets are beginning to distinguish between technological functionality and financial return. As disclosure will increase and pilot applications mature into business deployments, that distinction is more likely to turn into extra pronounced. Capital markets steadily get the path proper. Their extra widespread mistake is getting the timing incorrect. The historical past of infrastructure investing means that such miscalculations don’t turn into much less widespread as tasks develop bigger. They turn into extra consequential.

Metered Pricing and the Finish of Narrative Finance

One cause these points could turn into more and more tough to disregard is the business’s rising reliance on metered pricing. That pricing goes by totally different names. Token pricing fees clients based mostly on processing items consumed by AI fashions. Inference pricing fees based mostly on producing outputs from skilled AI fashions. Utilization pricing fees based mostly on how steadily clients use AI providers. API pricing fees based mostly on requests despatched via software program interfaces. No matter label you decide, the impact is similar: clients pay extra as AI consumption will increase.

The business is steadily shifting away from backed pilot pricing towards pay-as-you-go fashions, no matter whether or not fees are measured by tokens, inference, utilization, or API calls. That metered pricing turns the AI narrative right into a unit-economics downside.

For years, a lot of the AI dialogue has existed in a realm of strategic inevitability. AI would rework industries. AI would improve productiveness. AI would create new markets. Maybe it would. However metered pricing forces clients to ask a less complicated query:

What am I paying for? That query issues as a result of utilization can scale a lot quicker than many organizations anticipate. An enterprise could funds for a pilot venture solely to find that 1000’s of staff, automated workflows, customer-service programs, software-development instruments, and inside processes are consuming billions of tokens.

What initially seems cheap can rapidly turn into a big working expense. As metered pricing turns into extra widespread, analysts are evaluating income in opposition to depreciation schedules, energy prices, chip amortization, utilization charges, financing prices, and return on invested capital. The dialog shifts from innovation to economics, from chance to profitability, from Tech Bros’ narrative to unit economics.

That transition is usually the place speculative cycles encounter actuality. And when personal sector AI-driven financing crosses over into SEC-level scrutiny the anticipated AI crash could turn into a actuality.

IPO Disclosures and the Return of Public-Market Self-discipline

The identical dynamic applies to IPO disclosures. Personal markets can help kleptocrat PR narratives for remarkably lengthy intervals of time. Public markets are means much less forgiving.

IPO registration statements (SEC Kind S-1) require disclosure of dangers, buyer focus, cloud dependencies, income composition, capital commitments, related-party transactions, and quite a few different particulars that subtle personal buyers could already know however retail public buyers typically don’t.

As soon as these disclosures turn into accessible, buyers can start evaluating progress claims in opposition to financial actuality. How a lot income is recurring? How a lot is backed? How concentrated are clients? What are the true infrastructure obligations? What assumptions are embedded in future projections?

Solutions to those questions by themselves don’t essentially make AI much less helpful. They’ll make AI extra measurable. And measurable companies are sometimes much less thrilling than theoretical ones. That course of could speed up as a few of the largest AI firms transfer towards public markets.

There may be already substantial stress to incorporate firms corresponding to SpaceX and xAI in main inventory indexes as soon as eligibility necessities are met, and related stress is more likely to emerge for Anthropic and OpenAI if and after they turn into publicly traded. Index inclusion creates automated demand as a result of index funds and ETFs should buy the shares no matter valuation. But inclusion additionally brings better scrutiny, extra disclosure, and extra rigorous monetary reporting. As narratives give solution to numbers, buyers might be pressured to guage not simply technological potential, however precise revenues, margins, token consumption, infrastructure utilization, and return on invested capital. Markets are sometimes obsessed with potentialities. They’re significantly much less forgiving about measurable outcomes.

The Forecast Has Escaped Silicon Valley

Crucial improvement, nevertheless, could also be that AI forecasts are now not confined to know-how firms who’ve an astonishing capacity to persuade themselves of virtually something they are saying about themselves in a sort of folie à deux. There are others being pressured to take part within the hallucination.

Utilities are planning round AI forecasts. Transmission builders are planning round them. States are granting incentives round them. Pension funds are investing round them. Communities are reorganizing themselves round them because of the assault of the info facilities. A rising portion of the financial system is synchronizing across the similar assumptions relating to future AI demand.

That is the place the significance of forecasting being right or at the least not too overstated strikes past IPO finance. It turns into a query of public-risk allocation. Who advantages if the forecasts are right? Who bears the results if they’re incorrect?

Right here’s a clue: These usually are not the identical individuals.

Stranded Belongings and Political Danger

The length mismatch turns into considerably extra consequential when considered via the lens of stranded belongings. A stranded asset is an funding that continues to be bodily useful however fails to generate the revenues initially anticipated to justify its price. Within the AI context, that danger extends past chips and servers to incorporate knowledge facilities, transmission traces, substations, gasoline vegetation, water infrastructure, and different long-lived amenities being constructed to help projected demand. The know-how itself may match precisely as meant. The issue arises if adoption, utilization, or monetization develops extra slowly than forecast. In that state of affairs, billions of {dollars} of infrastructure may stay underutilized for years, producing returns far under expectations. The belongings don’t disappear; they merely turn into costly reminders that buyers appropriately anticipated the long run however arrived there too early.

The transmission tasks now proposed throughout the Texas Hill Nation illustrate the human dimension of stranded-asset danger. Landowners could lose water sources, farmland, privateness, and livestock grazing via easements and rights-of-way right this moment. Nobody can assure that the ensuing transmission capability will ever be absolutely utilized, and even wanted, on the timeline at present projected. If demand forecasts show overly optimistic, communities could bear everlasting penalties from infrastructure constructed to serve a future demand that arrives a lot later than anticipated—or by no means arrives in any respect in our lifetimes.

But the prevailing assumption is that right this moment’s infrastructure investments will ultimately be justified by tomorrow’s demand. Public documentation typically helps broad demand progress, however not particular utilization timelines for explicit knowledge facilities. The Worldwide Power Company tasks world data-center electrical energy consumption will double to about 945 TWh by 2030, whereas Goldman Sachs forecasts data-center energy demand rising 50% by 2027 and as a lot as 165% by 2030. However these are combination demand projections, not proof that specific knowledge facilities, transmission traces, substations, or gasoline vegetation will function close to capability on any particular schedule. World Sources Institute notes that forecasts fluctuate broadly, with Electrical Energy Analysis Institute estimating U.S. knowledge facilities may eat wherever from 4.6% to 9.1% of U.S. electrical energy by 2030—a variety equal to about 200 TWh. Brookings likewise emphasizes the opacity of data-center improvement and the necessity for better transparency. The lacking doc is the utilization curve: when every asset is anticipated to fill, below what contracts, and at what income yield.

In accordance with Bain’s 2026 examine:

Yearly, boards approve larger automation budgets. Yearly, CEOs log out on the following wave—robotic course of automation (RPA), then machine studying, then generative AI, now brokers. And yearly, the financial savings fall quick. Not catastrophically, not sufficient to kill the applications, however constantly, quietly, and by a margin that must be making executives uncomfortable.

Bain & Firm’s survey of 951 world firms finds that whereas 37% focused price reductions of 11% to twenty%, practically 40% of those that measured outcomes landed within the 0% to 10% bucket as a substitute (see Determine 1). The know-how labored. The worth didn’t arrive. And relatively than pausing to know why, 90% of those self same firms are actually growing their budgets once more—this time for AI brokers that may function with even better autonomy, complexity, and consequence.

These firms can, at the least theoretically, simply reduce or flip off the tokens. However in contrast to software program, knowledge facilities can’t merely be deleted as a result of they occupy land, they require roads, substations and transmission infrastructure. They eat water and so they alter landscapes.

If demand forecasts show optimistic, buyers could write down the belongings on monetary statements however the bodily belongings stay in communities that only some years earlier than have been offered a invoice of products. This creates a distinctly political type of danger as a result of whereas buyers can write down a stranded asset, communities must stay subsequent to it. A pension fund can take in an impairment cost, however a county can’t simply take away a half-empty hyperscale campus. A utility can revise forecasts, however a transmission hall stays.

A neighborhood that tolerated years of development, site visitors, noise, eminent-domain proceedings, utility upgrades, and panorama modifications could ultimately uncover that the promised financial exercise by no means absolutely materialized. At that time, monetary danger turns into political danger. The individuals who made the forecasts usually are not essentially the individuals who bear the results when these forecasts show incorrect.

The Public Has Already Develop into the Backstop

That is maybe the least appreciated facet of the whole AI buildout: The general public is already deeply embedded within the capital construction. Taxpayers help the system via grants, tax abatements, infrastructure spending, and government-backed financing. Ratepayers help utility investments. Pension beneficiaries help the system via retirement-fund allocations.

Index-fund buyers help it whether or not they actively select to or not as a result of a inventory will get added to an index like that S&P 500. To affix and index, an organization will need to have been worthwhile for the final 4 quarters as a complete and in the newest quarter particularly with a market capitalization of at the least $22.7 billion. It additionally should meet float and quantity standards. Firms should be based mostly in the US and commerce on one in every of a number of authorised U.S. inventory exchanges. S&P Dow Jones Indices, a enterprise run by S&P World, usually declares its picks on the second Friday of March, June, September, and December, and the listings often take impact after the shut of buying and selling the next Friday.

These are the final guidelines, however they are often waived. And guess who’s going to get them waived, partly from leverage and partly from retail demand.

The result’s a outstanding diffusion of danger. Many people concurrently occupy a number of positions within the AI financial system. They’re taxpayers. They’re ratepayers. They’re pension beneficiaries. They’re shareholders. More and more, they’re additionally the individuals dwelling subsequent to the infrastructure. The identical family could subsequently bear the dangers from a number of instructions concurrently. That’s uncommon. And it helps clarify why data-center controversies are rising in communities throughout the nation.

Too Large to Fail Redux: Why Nationwide Debt Issues

Due to China, the general public could finally get either side of the cut price: an argument for presidency fairness participation earlier than the upside is realized, and an argument for presidency rescue if the draw back seems. Why? As a result of China. AI might be framed as too strategically necessary to fail. Meaning taxpayers could also be requested to underwrite infrastructure, take in losses, help failing investments, and protect nationwide competitiveness, whereas additionally being informed that public fairness stakes are essential to seize a few of the upside from an business constructed with public help.

The AI bailout debate is now not hypothetical. The Open Markets Institute has urged policymakers to organize for calls for to rescue giant know-how firms if the AI bubble bursts, warning that national-security arguments and “too necessary to fail” rhetoric could also be used to socialize losses. The strongest bailout case can be framed round China, strategic compute capability, grid infrastructure, and protection readiness. The strongest objection is that personal buyers captured the upside whereas taxpayers, ratepayers, and communities are requested to soak up the draw back. The probably kind could also be much less a dramatic rescue than a slow-motion bailout via subsidies, ensures, procurement, and infrastructure help.

Senator Bernie Sanders’s latest proposal that the federal authorities obtain a considerable fairness stake in AI firms differs from a conventional bailout in an necessary respect. A bailout usually socializes losses after personal buyers have already acquired the advantages of possession and management. An fairness participation mannequin makes an attempt to align public danger with public reward by giving taxpayers a share of future income, appreciation, and dividends in change for the infrastructure, subsidies, analysis funding, regulatory help, or different public sources that assist make these firms profitable. In concept, the federal government turns into an investor relatively than merely a guarantor of losses. Critics argue this resembles partial nationalization, whereas supporters contend it prevents the general public from bearing prices with out sharing within the upside.

However taxpayers and ratepayers are already functioning as junior capital suppliers maybe with out realizing it. If rural landowners lose easements, ratepayers fund transmission upgrades, and governments present tax abatements to help AI infrastructure, Then the general public could already be absorbing parts of the draw back danger. Sanders’s proposal is basically an argument that if the general public is already underwriting the venture, the general public ought to obtain fairness relatively than merely

The AI bailout debate is now not hypothetical. The Open Markets Institute has urged policymakers to organize for calls for to rescue giant know-how firms if the AI bubble bursts, warning that national-security arguments and “too necessary to fail” rhetoric could also be used to socialize losses. The strongest bailout case can be framed round China, strategic compute capability, grid infrastructure, and protection readiness. The strongest objection is that personal buyers captured the upside whereas taxpayers, ratepayers, and communities are requested to soak up the draw back. The probably kind could also be much less a dramatic rescue than a slow-motion bailout via subsidies, ensures, procurement, and infrastructure help.offering help.

The extra probably consequence just isn’t a sudden, headline-grabbing AI bailout. It’s a slow-motion bailout unfold throughout tax abatements, backed energy, accelerated allowing, ratepayer-funded transmission, federal mortgage ensures, protection procurement, public-private partnerships, and national-security exceptions. No single intervention could appear to be a rescue. Taken collectively, nevertheless, they’ll shift draw back danger from personal buyers to taxpayers, ratepayers, landowners, and native communities lengthy earlier than anybody admits that the bubble has burst.

That may be very totally different from a bailout. A bailout often happens after losses emerge. An fairness participation mannequin makes an attempt to assert a share of features earlier than they happen—nevertheless it essentially means sharing losses if the underlying assumptions show incorrect. An AI crash would imply each shedding the inventory, the tax abatements, and provides them a bailout. That is why you don’t get funding recommendation from a socialist.

There may be one ultimate dimension to this a part of the story. On the peak of the dot-com increase, gross federal debt stood at roughly $5.7 trillion. On the onset of the worldwide monetary disaster, it was roughly $10 trillion. In the present day it exceeds $38 trillion. That doesn’t make a disaster inevitable. It does, nevertheless, cut back the margin for error.

Earlier speculative episodes occurred when the federal authorities possessed significantly better fiscal flexibility. The present AI buildout is happening in a basically totally different surroundings. That issues as a result of many contributors nonetheless implicitly assume that public establishments retain the identical capability to soak up errors that existed throughout prior cycles.

That assumption deserves scrutiny as a result of they don’t.

The Actual Query

The traditional AI debate focuses on know-how. The extra necessary debate could concern forecasts. The market is making an attempt to assign a gift worth to a future demand curve whose form, magnitude, timing, and economics stay unsure. Utilities are planning round that curve. Governments are subsidizing round that curve. Pension funds are investing round that curve. Communities are reorganizing round that curve.

The query is now not whether or not buyers have priced AI appropriately. The query is whether or not the nation has, or possibly even when the world has.

If the forecasts show considerably right, the present buildout could finally be considered as some of the vital infrastructure mobilizations in trendy financial historical past. If they don’t, the adjustment is not going to be confined to Silicon Valley steadiness sheets. It can seem in utility payments, public budgets, pension portfolios, tax revenues and environmental liabilities. And native communities that have been requested to soak up everlasting modifications based mostly upon assumptions that finally didn’t materialize. That’s the essence of forecast danger.

The individuals making the forecasts are rarely the individuals who bear the results when they’re incorrect.

{kind=link}